In Part I of this two-part series I discussed the pros and cons of 15 and 30 year mortgage terms, which are the two most common types. The main benefit of shorter loan terms in general is less money paid in interest over the course of the loan. The main benefit of longer loan terms in general is a lower monthly payment, which frees up funds to use in other pursuits.

Debt-averse advocates will argue that shorter loan terms (or no loans at all) will allow you to have fewer monthly financial obligations, which increases financial freedom. Pro-debt advocates will argue that debt at a low-enough interest rate can be leveraged in order to make money elsewhere which negates the losses to interest.

Most debt-averse advocates such as Dave Ramsey will usually allow for a home mortgage because homes are pretty expensive and saving up to buy one in cash can take quite a while, during which time one would inevitably have to rent a residence and probably pay much more in the long run. Ramsey, however, only recommends for mortgage terms of 15 years or less, under the assumption that the monthly payment is less than 25% of an individual's take-home pay.

This "conservative" approach to a mortgage is questioned by the less debt-averse crowd, and possibly for good reason. I included "conservative" in scare-quotes because, and this is perhaps a spoiler to my conclusion of this article, I don't actually think the 15 year mortgage term is more conservative in most cases. A 30 year mortgage could actually be argued as the less risky approach.

To come to this conclusion, I analyzed data for average new home prices, inflation rates, and S&P 500 returns since 1963 (this was the earliest I could find home price statistics). I looked at the price of new homes because I figured this was a more consistent metric than average price of home sales, because homes can change in value for a variety of reasons.

As it turns out, though, the home price doesn't really make that much of a difference, because this experiment is not particularly concerned with how the house appreciates.

The Setup: Two Parallel Universes

The question I sought to answer was this: if someone buys a house with a fixed interest rate and they invest any extra income in an S&P 500 index fund, would they have been better off after 30 years with a 15 or a 30 year mortgage?

For both circumstances, at the end of 30 years the person will have a paid-off house and some amount of money in investments. The only metric to then determine is what exactly is meant by "better off"? For initial purposes I will define "better off" as the person who has the most money in investments minus the amount they paid for their home (principle plus interest).

Disclaimer: I am not a financial adviser, I am just an electrical engineer who knows his way around a spreadsheet and looked up a few datasets on the internet. The conclusions I make are based on past data, and in the world of finance nothing is guaranteed. So take the following graphs and conclusions with a grain of salt, and think twice before making major financial decisions.

For the following data, one thing I am not taking into consideration is taxes. The reason for this is because taxes are heavily dependent on individual financial situations and would be difficult to generalize. This would already give a slight edge to the 15 year mortgage term because mortgage interest is tax-deductible (although the recent tax code changes make this less advantageous for moderately priced homes).

Get ready for a barrage of charts and graphs. For all the data below, I'm assuming the following:

-A person is buying an average-priced new house for the given year

-The house payment on a 15-year mortgage at the time of purchase is 35% of their take-home pay (more risky than the Dave Ramsey suggestion)

-The same house is financed at both 15 years and 30 years (in two separate parallel universes where everything else is equal)

-The interest rates specified on the charts are with respect to the 15 year mortgage. For the 30 year mortgage, the interest rate is 0.5% more (since 30 year mortgages always have higher rates, and from my research they are usually about 0.5% higher)

-For the case of the 15 year mortgage, the person pays the minimum payment every month until the house is paid off after 15 years. The person then starts investing their monthly payment in an S&P 500 index fund

-For the case of the 30 year mortgage, the person pays the minimum payment every month for 30 years until the house is paid off. They invest the difference of the 15 and 30 year payment in the S&P every year.

-In some cases, both people may invest an extra percentage of their take-home pay each year

-At the end of 30 years, I assessed each person's assets minus costs, i.e. how much they have in investments minus how much they paid for their home (principal + interest). The final value of the home is not included, as it will be the same in both cases

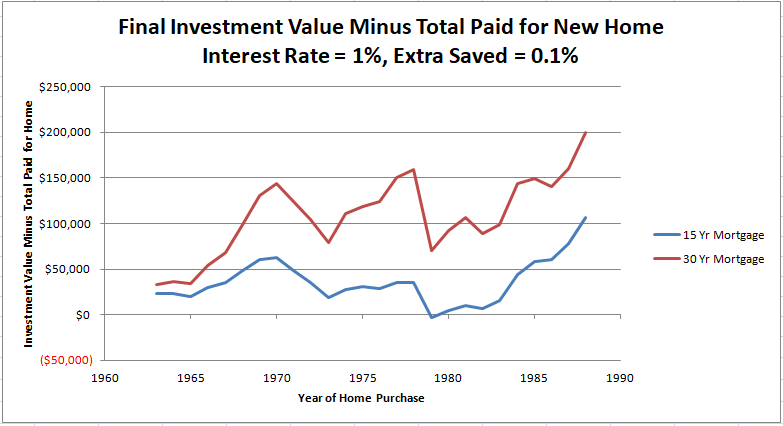

So here we go! Let's first look at an absurdly low interest rate of 1%:

The relative amounts of each of these lines will change with the coming graphs, but the general shape of them will be pretty consistent. You'll probably notice a big dip in both plots at the 1978 purchase year. That's because guess what happened 30 years later? That's right, the largest financial crash since the great depression! As you can see, it hit the 30 year mortgage worse since that case had more money in investments, but it was still well ahead of the 15 year mortgage (which actually came out in the negative).

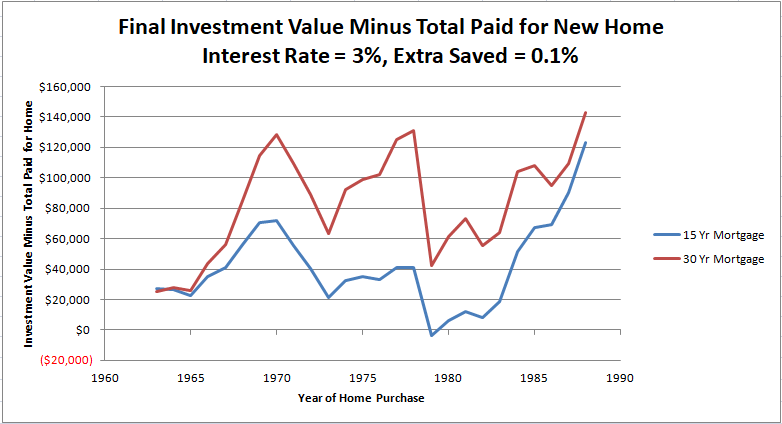

Let's check out a 3% interest rate!

The 30 year mortgage still wins every year, but the 15 year is coming back with a vengeance in recent years. This makes sense, as the 15 year mortgage starts to have a greater portion of their investments during the recession, which means their recovery from it will be more pronounced.

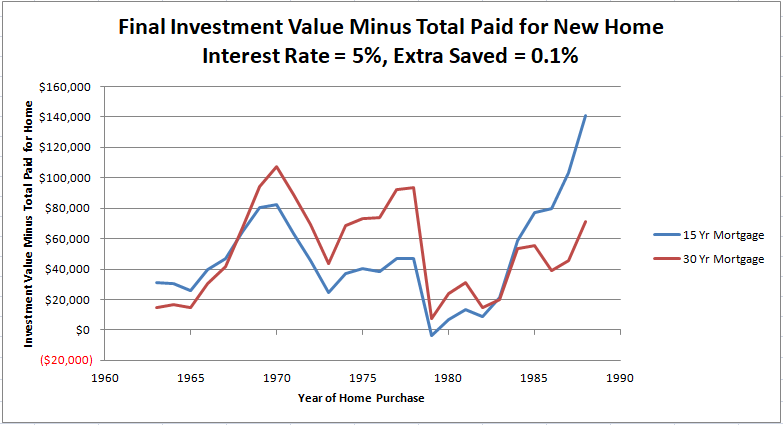

Alright, let's see about 5%!

Now we start to see the revenge of the 15 year mortgage. For the early and more recent years, the 15 year mortgage comes out on top, although the 30 year mortgage still wins in 58% of the years.

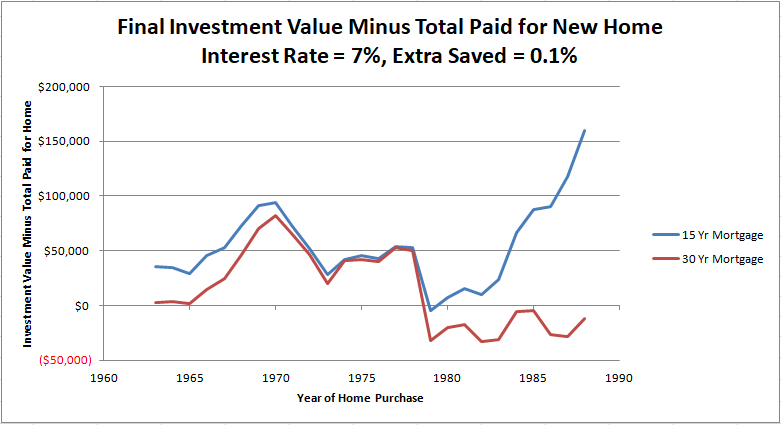

Alright, so what about 7%?

So now the 15 year is the clear winner, and by quite a bit for recent years. This is fairly expected for around a 7% interest rate, as the S&P averages about a 7% return, and the volatility of the market in the past decade exacerbates the difference between the two options.

What have we learned so far? Mostly that a 30 year mortgage is the better option if the interest rate is below about 5.5% in most cases. I can't extend the data out any more, but my guess is that the 15 year will keep winning for higher interest rates in the coming years, but gradually slow down and perhaps give way to the 30 year once more if a market correction occurs.

But What About Risk?

The above charts act as a good baseline for the 15 vs. 30 year debate, but they both assume that a person has a consistent income that increases with the rate of inflation every year. While some people can probably expect their salary to increase at or above the rate of inflation every year for 30+ years, this is probably not going to be the case for most people, and is a risky thing to assume for one's self.

According to NGPF, Baby Boomers experienced 5.6 periods of unemployment on average between ages 18 and 48. That's quite a few, and I'm not sure if this includes people in short-term unemployment because they are willingly changing jobs, but in any case it's a lot of times that their finances were potentially strained. Even worse, if someone loses their job during a recession, when unemployment is high, then their likelihood of being unemployed for longer than 1 year is almost 1 in 10.

And it's not just unemployment that can financially strain you. Many people do not have stable, salaried jobs, and may have large fluctuations in income each year. Life is also full of unexpected expenses, and the risk of these definitely increases with home ownership.

This is why most financial gurus recommend having an emergency fund, although the amount can vary. There are also some differences in opinion as to whether or not an emergency fund should be in savings or investments.

In order to assess risk for our 15 vs. 30 year mortgage terms, I'll assume for the sake of argument that each case does not have an emergency fund in savings, and instead must rely entirely on their amount in investments. While this is pretty risky, having just a 3-6 month emergency fund may be fairly risky as well, since there's no guarantee that an unemployment term will only last 6 months.

I'll now define what I call a "danger year", which would be a year in which a person's annual expenses are greater than the amount they have in investments. This would mean that they wouldn't be able to last an entire year without their income if they relied on just investments.

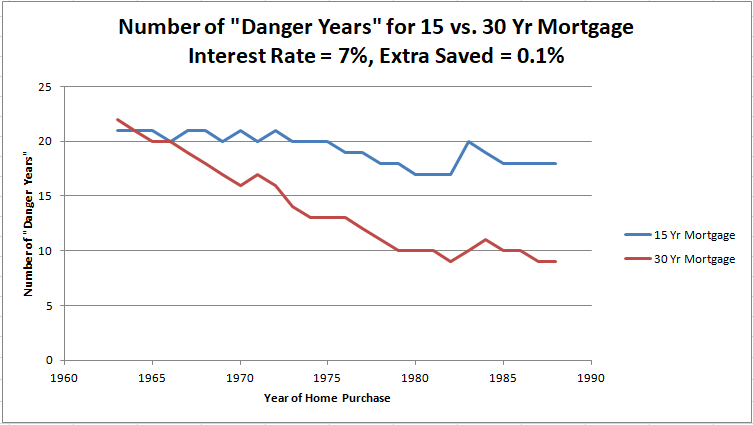

If we revisit the case in which the interest rate was 7% (which was a clear winner in terms of final value for the 15 year mortgage), then things change a bit when you account for "danger years"...

As we can see the 15 year mortgage has 16-21 "danger years" for most cases, which is because the savings rate is basically 0%, so every year in which you have that 15 year mortgage is a year that things could go badly, and it takes several years of investing after that to build up a nest egg. We can also see that the 30 year is about the same as the 15 year for past years, but shows some promise in recent years.

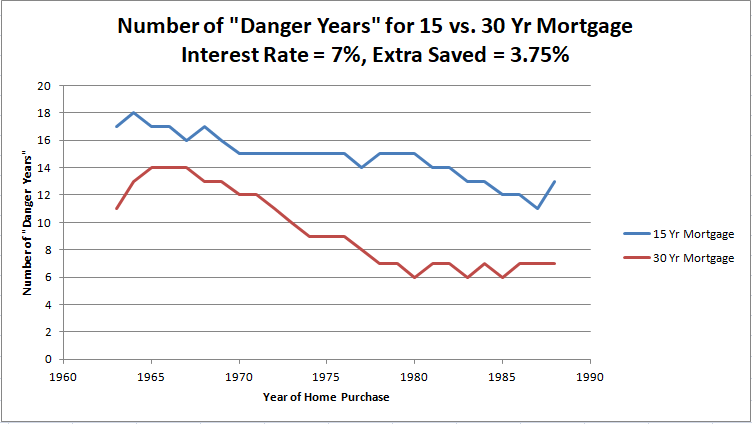

This is perhaps unfair to the 15 year mortgage, since one would assume that there would be at least some savings in excess of normal spending. So let's see what happens if we can save a small 3.75% of your take-home pay each year...

This makes things slightly better for the 15 year mortgage in recent years, but it also makes things much better for the 30 year mortgage, allowing it to win comfortably every year.

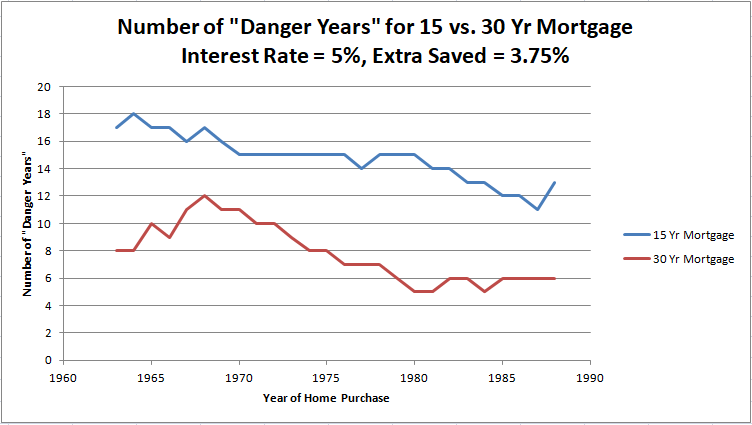

If the interest rate is more favorable, things get even better for the 30 year...

If recent trends hold true, then the 30 year mortgage has 6+ fewer years of financial vulnerability than the 15 year. That's fairly significant if you ask me.

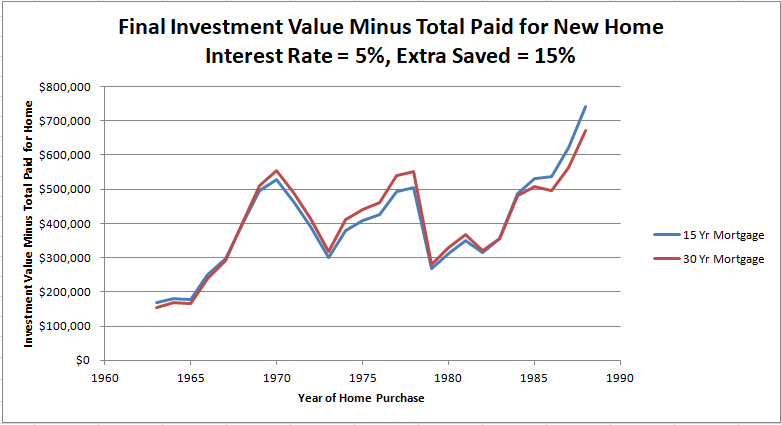

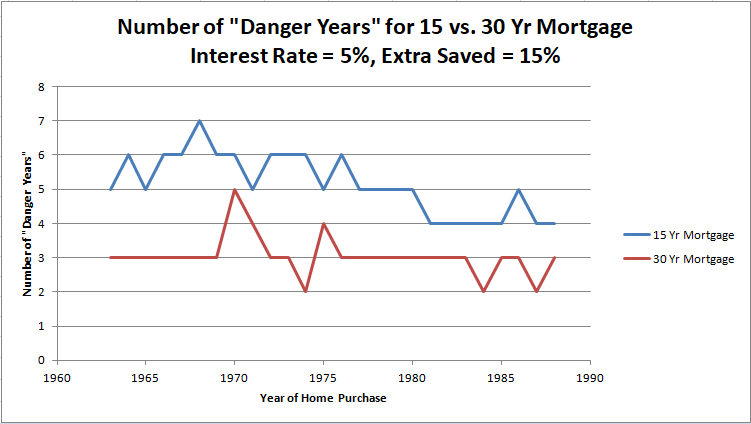

As the savings rate increases, things become more equal for each term. If you're able to save 15% every year for a 5% mortgage, then the plots look like this:

With a large savings rate, the final value plots become nearly identical, and the number of danger years are nearly equal, with the 30 year beating the 15 by one or two years normally.

Conclusion

What does all this mean? Well, if you get a decent interest rate (less than about 6%) and you can save and invest a good percentage of your income every year, then it really doesn't matter.

If, however, you can only save a little bit of your income, then you probably shouldn't buy a house that expensive, but if you do then you should probably go with a 30 year mortgage.

In fact, I'll make the argument that regardless of interest rate, and regardless of how much you can save, you should always get a 30 year mortgage. If interest rates are high, then you can always prepay on a 30 year and get it paid off sooner (which means less interest paid). If times are tough, you can just go back to paying the minimum and the repo man won't come knocking. For a 15 year mortgage, you're stuck with that higher monthly payment, and as long as you have it, you're more financially vulnerable.

There is, of course, one final argument that could be made for the 15 year mortgage: it acts as a sort of "forced savings account". If you're the kind of person that struggles with saving, and willingly spends every extra penny you have, then a 15 year mortgage with its higher monthly payment forces you to live on less for 15 years. Assuming your house appreciates, this money you put away on it can potentially be realized later.

I don't, however, think that this is a great argument. If you don't have the self control to save the extra money on a 30 year mortgage, then what makes you think that you'll have the discipline to save your entire monthly payment once the mortgage is paid off? Your problems go deeper than mortgage terms.

At the end of the day, how financially secure you are has more to do with what your savings rate is than anything else. And even with market fluctuations, investing your money in an index fund is not a huge long-term risk, and the losses you would experience by not investing would be far greater than any market losses you might incur over a long period.

Keep in mind, I'm just a guy who threw all these numbers together pretty casually, so feel free to double-check my work and let me know if there is anywhere I messed up or anything I didn't take into account...